The Problem with Savings Accounts

Most people park money in savings accounts, even when they know they’ll need it for EMIs, a purchase, or expenses in a few months. It feels safe, but the problem is returns.

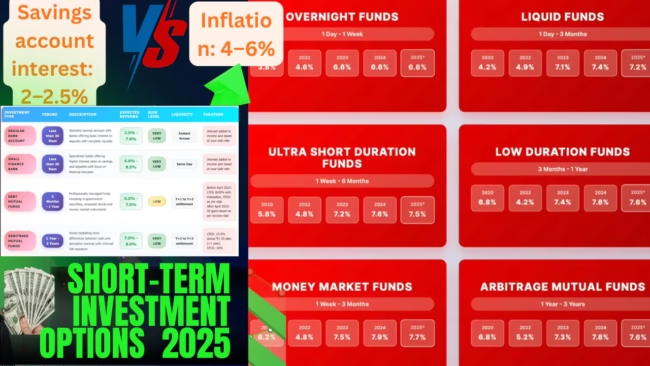

- Savings account interest: 2–2.5% (average across banks).

- Inflation: 4–6% (recent years).

That means your money loses value in real terms. Example:

| Amount in savings | Interest earned (2.5%) | Value after inflation (5%) | Real loss |

|---|---|---|---|

| ₹1,00,000 | ₹2,500 | ₹95,000 | -₹2,500 |

So, if you keep ₹1 lakh for a year, you end up with less purchasing power.

For very short needs (a few days or a week), savings accounts are fine because of instant liquidity. But for anything beyond 30 days, you should look at better options.

In this article, I’ll share strategies I’ve personally used and researched, explain how each option works, and show you Best Short-Term Investment Options in India 2025 can beat savings account returns.

By the end, you’ll know:

- Why keeping money in savings accounts can cost you.

- Which safe short-term investment options are best for 3 months to 3 years.

- How to invest in debt and arbitrage mutual funds smartly.

Table of Contents

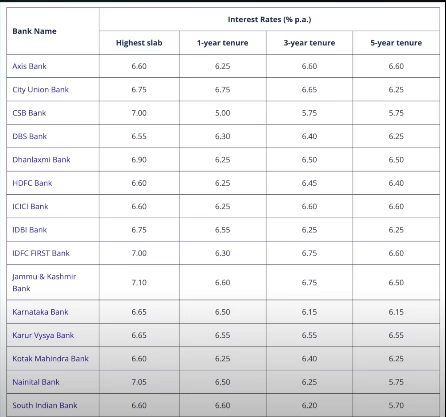

Option 1: Fixed Deposits (FDs)

FDs are the traditional go-to for short-term savings.

- Public/private banks: 6–7%

- Small finance banks: 7.5–8.4% (higher for senior citizens)

Pros:

- Safer than markets.

- Predictable returns.

Cons:

- Lock-in. Premature withdrawal = penalty.

- Interest is fully taxable.

- Insurance limit of ₹5 lakh per bank under RBI rules.

Example:

₹1 lakh in a 1-year FD at 7% earns ₹7,000. After 20% tax, you keep only ₹5,600.

Verdict: Good if you don’t need the money early.

Option 2: Debt Mutual Funds

Debt funds invest in bonds and short-term securities. They work like FDs but are more flexible.

Types:

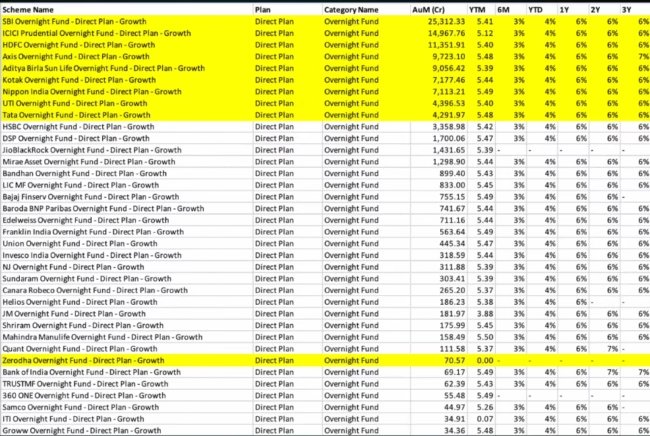

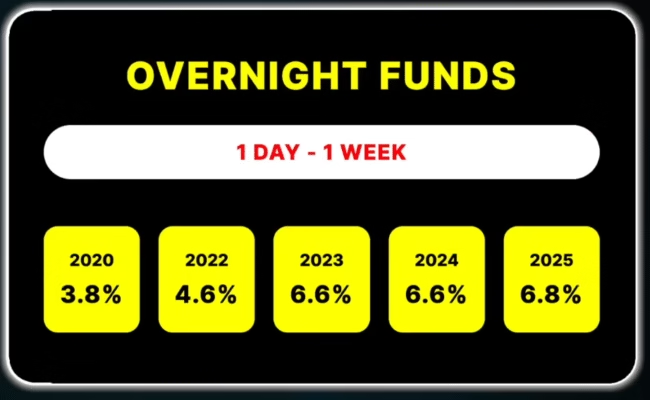

- Overnight funds → 1-day maturity, ~6.5% return.

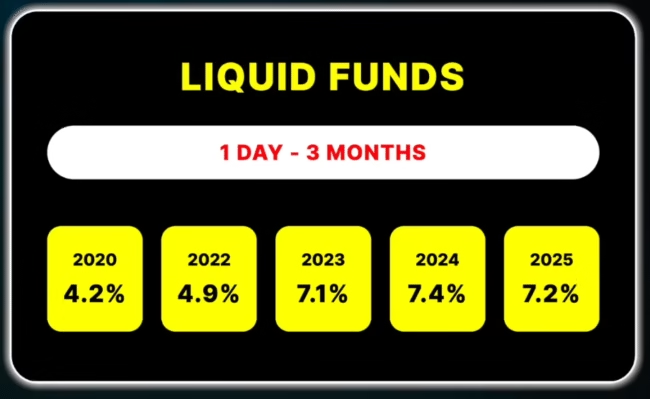

- Liquid funds → Up to 91 days, ~7% return, low risk.

- Ultra-short duration funds → 3–6 months horizon.

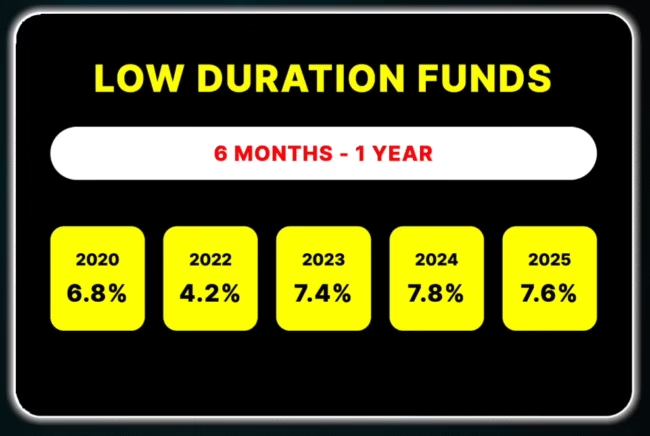

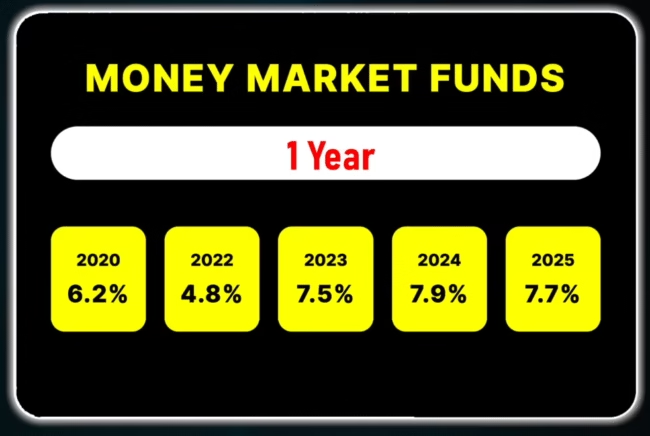

- Low duration / Money market funds → 6–12 months horizon.

Pros:

- Easy exit. Most liquid funds have no penalty after 7 days.

- Better liquidity than FDs.

- Diversified portfolio lowers risk.

Cons:

- Returns not guaranteed.

- Taxed like FD interest at your slab rate.

Example:

₹1 lakh in a liquid fund grows ~₹7,000 in a year. Tax at 20% = ₹5,600 net (same issue as FD).

But, you can withdraw anytime without penalty.

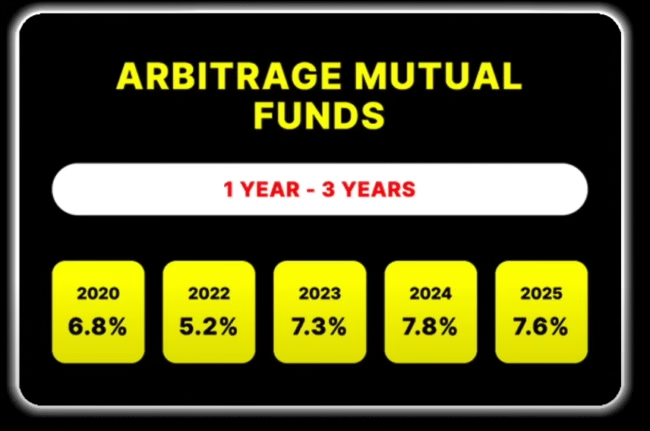

Option 3: Arbitrage Mutual Funds

Arbitrage funds are technically equity funds but behave like debt. They make money from price gaps in cash and futures markets.

- Returns: ~8% annually

- Risk: Low (since positions are hedged)

- Liquidity: Easy redemption, like other mutual funds.

Arbitrage Mutual Funds is one of the Best Short-Term Investment Options in India 2025

Tax benefit:

- Held >1 year = Long-term capital gains (LTCG) taxed at 12.5% only.

- Much lower than slab taxation on FD/debt fund interest.

Example:

₹1 lakh in arbitrage fund at 8% = ₹8,000.

Tax at 12.5% = ₹7,000 net.

Compare this to FD/debt funds where net is ~₹5,600.

Verdict: Best for 1–3 year horizon, especially if you’re in higher tax brackets.

Option 4: Direct vs Regular Mutual Fund Plans

When you invest in mutual funds, you can pick:

- Direct plan → Expense ratio ~0.7%, no middlemen.

- Regular plan → Expense ratio ~1.3–1.5%, commission included.

Over time, that small % makes a difference.

Example:

₹1 lakh in liquid fund:

- Direct plan (7% return) = ₹1,07,000 after 1 year.

- Regular plan (6.3% return) = ₹1,06,300 after 1 year.

Extra ₹700 just because of plan choice. Over 10 years, the gap compounds.

Comparison Table – Which Option Fits Best?

| Investment option | Returns (annual) | Liquidity | Tax treatment | Risk | Best for |

|---|---|---|---|---|---|

| Savings account | 2–2.5% | Instant | ₹10,000 exemption under 80TTA | None | <30 days |

| Fixed deposit | 6–8% | Penalty on early exit | Fully taxable | Low | 6–36 months if stable |

| Debt mutual funds | 6.5–7% | Easy exit (after 7 days) | Fully taxable | Moderate | 3–12 months |

| Arbitrage funds | ~8% | Flexible | 12.5% LTCG after 1 year | Low | 1–3 years |

FAQs on Best Short-Term Investment Options in India 2025

Q. What is the best short-term investment option in India 2025?

For <30 days → savings account. For 3–12 months → debt mutual funds. For 1–3 years → arbitrage funds.

Q. Are FDs still worth it?

Yes, but only if you don’t plan to withdraw early and are okay with paying full tax.

Q. Which option is safest?

Savings accounts and FDs are safest. Among mutual funds, liquid and overnight funds are very low risk.

Q. Why not just keep money in a bank?

Because inflation eats away your real returns.

Conclusion: Best Short-Term Investment Options in India 2025

Savings accounts are fine for a week or two. Beyond that, your money works harder elsewhere.

- FDs = safe, but taxable and less liquid.

- Debt funds = flexible, short-term parking.

- Arbitrage funds = best balance of return + tax efficiency for 1–3 years.

Pick based on how long you can stay invested and your tax bracket. That way, you stop losing money to inflation and start earning more from your short-term savings. Arbitrage Mutual Funds is one of the Best Short-Term Investment Options in India 2025 if you plan for more than a year.

Click here to explore all articles on FinanceWithXpert

📲 Join our finance community:

COMMENTS